Haven for Hope sets the standard for helping those who are experiencing homelessness. With their partners and numerous volunteers, they have provided care to 40,000 individuals since they began operations in 2010. I was fortunate to have the opportunity to conduct a cost-benefit analysis of Haven for Hope covering the period of its founding in 2007 through 2019. The benefits measured in the study included the economic and fiscal impacts of Haven for Hope operations, the economic and fiscal impacts of the volunteers at Haven for Hope, benefits of reduced crime, benefits of providing school stability to children, and the benefits of medical care, housing, and other care services. Measured against the costs of developing and operating the facilities and programs, the net benefits the organization provides to the community are impressive.

Net benefits to the community ranging from $2.9 billion to $8.2 billion with an average of about $5.6 billion.

Benefits to the community per dollar spent ranging from $15.29 to $41.89 with an average of $28.72.

Haven for Hope has not only had profoundly positive impacts on those they serve, but the effects on the quality of life and the economy extend throughout San Antonio. The report discussing the impacts in more detail and documenting how the analysis was conducted can be found here.

I recently gave a speech to the Alamo Chapter of the Government Finance Officers Association of Texas in which I shared my thoughts on the state of the economy and my forecast for the San Antonio economy in 2023. In short, I am about as confident as one can be that we will have a recession in 2023. The biggest uncertainty about the forecast concerns how long the recession will last and how deep it will be. At this point my thought is that the economy will not experience a big decline, and the decline will be for a relatively brief period of time.

Although I am by no means the only economist who is predicting a recession, it seems somewhat odd calling for a recession at this point, since employment growth is strong, the unemployment rate is low, and gross domestic product is still growing. However, there are some key indicators that are pointing toward a recession. One of the main indicators is the yield curve, which has not been this persistently inverted in forty years. Employment growth, while still strong, is declining, and the unemployment rate appears to have hit its bottom. Consumer spending is starting to slow as the large increase in savings due to the various pandemic stimulus programs has been depleted. Delinquency rates on credit cards are also rising indicating consumers are under some financial stress. Private domestic investment is starting to decline, as it has done before every recession since 1980. The housing market has started to soften, as have other lending activities. These trends are what we expect to see as the Federal Reserve has raised their Federal Funds Rate a large amount in a short period of time to try to get inflation under control with the ultimate goal of also keeping the economy on its growth path. In other words, it is trying to execute a “soft landing.” In my reading of the data going back to the recession at the beginning of the 1970s, the Federal Reserve has not been successful at executing a “soft landing,” so I am not confident that they will be successful this time. This is not meant to discredit the Federal Reserve; it is just an extraordinarily difficult task to accomplish.

Given the direction all of these indicators are pointing, I am projecting that employment growth in San Antonio will be flat to down about 1.0%, and the unemployment rate will rise to 4.5-5.0% in 2023.

The San Antonio economy has bounced back from the pandemic-induced recession quite nicely, and I believe the economy will likely continue to show growth at or slightly above its long-term trend in 2022. I project employment growth this year to be in the range of 2.2-2.7%, and the unemployment rate will continue to decline to about 3.5-4.0%. The data, trends, and potential factors that I am seeing in my crystal ball that form the basis for this forecast are discussed in the rest of this post.

After a quick rebound from the pandemic-induced recession, the San Antonio economy has moved toward its more long-term average growth rate in employment. This is somewhat against the pattern seen in the other major metropolitan economies across Texas, as they have continued to maintain historically strong growth. This is especially the case for the Austin economy. These patterns are evident in the following chart showing the year-over-year employment growth. Even though many of these areas have continued to experience such strong growth, it is clear that there is a sizable gap between them and the Austin economy.

As shown in Chart 2, the Austin economy grew 8.11% percent in December, which was still substantially larger than the second-fastest growing region – Dallas – at 5.82% and Fort Worth, the third fastest growing region at 5.02%. The San Antonio economy grew 2.87% in December – the slowest among the major metropolitan regions and below the growth rate across the state of 5.08% and the U.S. at 4.52%.

The large disparities in the growth of the Austin economy relative to San Antonio, and the other major metropolitan economies in Texas for that matter, is worth exploring, and I will have a post on that soon. For now, I want to focus on San Antonio.

Chart 3 shows the year-over-year employment growth by month across broadly-defined industries from January 2019 through December 2021 for San Antonio. As expected, the hospitality industry took the largest dive during the lock down followed by the professional services industry. These two industries have also had the largest immediate recoveries, along with the other services industry.

Chart 4 and Table 1 show the employment growth by industry from the depth of the pandemic-induced recession in April 2020 to a year later in April 2021, i.e., from trough to peak, and then for the remainder of 2021. It needs to be kept in mind that these are similar lengths of time, but it is clear from these numbers that the growth rates across almost all of the industries in San Antonio have slowed considerably. The manufacturing, construction and mining, and education and health industries have seen their growth basically stall or even turn slightly negative in the last three quarters of 2021. The one exception is the hospitality industry that not surprisingly continues to experience growth far above average.

Table 2 compares employment growth in San Antonio over its history leading up to the pandemic (Jan. 1991-Dec. 2019) to the growth rates across industries over the past year. Overall employment growth in 2021 was 2.87%, a bit above the historical average of 2.37% growth. Five of the ten industries – manufacturing; trade transportation, and utilities (TTU); professional services; hospitality; and other services – continued to grow at above average rates in 2021. Not too surprisingly, the hospitality industry continues to lead the growth with a rate of 10.87% in 2021 – far above the industry’s historical average. Only two industries experienced declining growth in 2021 – construction and mining and information. As shown in Chart 3, the declining growth in the information industry is a regression back to the mean based on recent history. Not to give away too much of the punch line for my next post, but this explains, in part, the difference in growth rates between Austin and San Antonio.

I expect these overall slowing trends in employment growth to continue through 2022 in San Antonio. Some of this is just going to be a regression back to the mean from the large growth rates as the economy recovered from the pandemic-induced recession. The structure of the San Antonio economy is an additional reason, and the potential effects of growth in the global and national economies will also play a role, as discussed below.

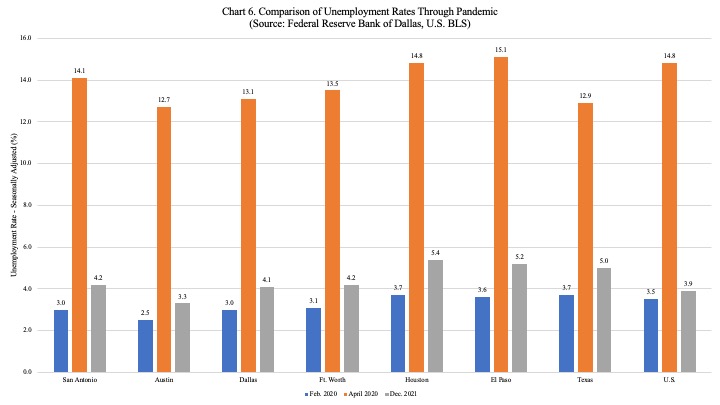

Similar to the pattern in the other major metropolitan Texas economies and across the state and U.S, the unemployment rate in San Antonio has steadily declined after the precipitous fall following the re-opening of the economy ending 2021 at a rate of 4.2% (see Chart 5). As shown in Chart 6, San Antonio had one of the lowest unemployment rates among the major metropolitan economies in Texas before the pandemic at 3.0%. However, San Antonio experienced one of the largest surges in its unemployment as it climbed to 14.1% in April 2020 at the depth of the recession, but as noted, unemployment has been consistently declining and is similar to the rate in Dallas (4.1%) and Fort Worth (4.2%). The unemployment rate in San Antonio is also lower than the statewide rate at 5.0%, but it is a bit higher than the U.S. unemployment rate at 3.9%. Compared to San Antonio, the unemployment rate in Austin was 0.9 percentage point lower at the end of 2021 at 3.3%. The strong economic growth since April 2020 has surely been the main driver pushing unemployment rates down, but it should be kept in mind that at least part of this decline may be due to the decline in the labor force participation rate due to the Great Resignation phenomenon. In fact, while the labor force participation has been increasing, it is still below the pre-pandemic rate of 63.4% in February 2020 for the U.S.

These structural changes in the labor market are one of the risk factors to this forecast. I can see these changes potentially having both positive and negative effects on economic growth. If the labor market adjusts to these changes fairly quickly and workers fill the jobs at higher pay and with enhanced benefits, this could serve as a boost to overall economic growth. However, if the current trend continues for an extended period of time, this could continue to exacerbate the shortages in many markets and serve to dampen economic growth. These adjustments in the labor market may be forestalled in industries where there is a relative paucity of benefits, such as paid sick leave. If the shortages causing the rapid increase in the inflation rate do not diminish in the near future, the persistent inflation at relatively high rates will also likely be a deterrent to growth in and of itself. In response to this, the Federal Reserve has sent strong signals that it will most likely be raising interest rates several times this year, which will also serve to slow the economy some. There could also be bubbles in many asset markets, such as the stock and housing markets, and if one or more of those bubbles burst, they might also cause the economy to pause a bit, even if it does not push it into a recession. The strong economic growth was, at least in part, driven by the federal government stimulus, and with that coming to an end, consumer spending is likely to move back into a more typical pattern over time causing a moderation in U.S. economic growth. It is also likely that growth in the global economy will also slow this year because of similar trends, and the economic effects of the war in Ukraine may also slow global economic growth a bit. Overall, it seems these various factors combined with the structure of the San Antonio will mean the local economy will continue to grow fairly strongly in 2022 but at a slower rate than in 2021.

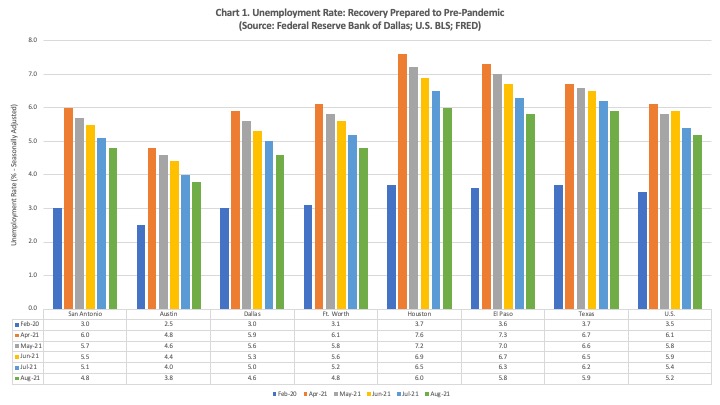

The unemployment rate continued its decline in August across the major metropolitan economies in Texas and across the State and U.S. as the recovery from the economic effects of the pandemic continue (see Chart 1). In San Antonio, the unemployment rate declined to 4.8%, This is 1.8 percentage points above the pre-pandemic level, so while the economy is certainly recovering, there is still a ways to go. San Antonio has the third lowest unemployment rate compared to the other major metropolitan economies in Texas with Austin having the lowest at 3.8%. The unemployment rate in Texas stood at 5.9%, a bit higher than the unemployment rate for the U.S. at 5.2%.

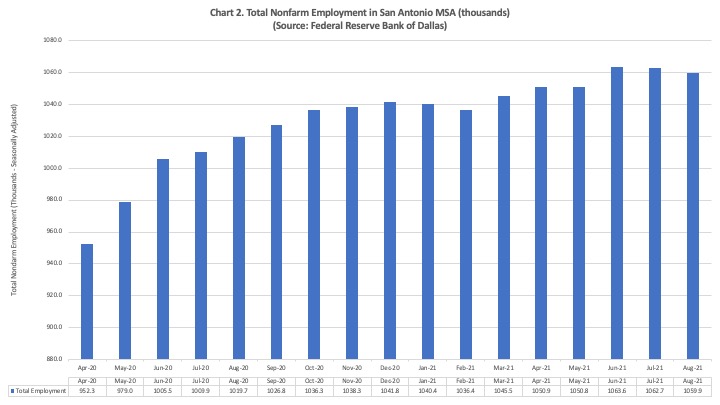

However, the total level of employment in San Antonio declined in July and August, as shown in Chart 2. This indicates to me that at least part of the decline in the unemployment rate in San Antonio may be due to people dropping out of the labor force and therefore, no longer being counted in the unemployment rate. This is also occurring in some of the other major metropolitan economies across the state.

While there have been monthly declines in total employment the past couple of months, the year-over-year growth rates in employment continued to be strong in August with growth in San Antonio coming in at 3.94% (see Chart 3), a good bit above the average historical growth rate in the region of about 2.3%. However, these growth rates continue to decline across most regions in the state, as well as across the entire state of Texas and the U.S. This is likely due to a regression to the mean as the recovery continues and some pull back in consumer spending due to the Delta variant. Another possible factor is the lag in business travel due to the pandemic. This especially affects those local economies with large leisure and hospitality industries like San Antonio because the convention activity is not filling in for the decline in leisure travel as the new school year began.

If we can keep making strides against the pandemic, growth should continue into the near future. This does not mean the year-over-year growth rates will increase, as they will likely tend to move more toward their long-term average rates in the respective areas as the economy gets closer to full employment. The sustained growth will also continue to push the unemployment rates down, especially as the structural unemployment is reduced.

The unemployment rate in the U.S. was recently reported to be at 14.7% in April. Here is a link to the full report released by the U.S. Bureau of Labor Statistics. It is somewhat lengthy, but as always, it is worth a quick look, especially since this report contains some insightful information beyond the headline unemployment rate.

One insight is the difficulty in being able to correctly capture the data due to the unique situation caused by the pandemic. This is highlighted in the following statement from the report.

However, there was also a large increase in the number of workers who were classified as employed but absent from work. As was the case in March, special instructions sent to household survey interviewers called for all employed persons absent from work due to coronavirus-related business closures to be classified as unemployed on temporary layoff. However, it is apparent that not all such workers were so classified.

If the workers who were recorded as employed but absent from work due to “other reasons” (over and above the number absent for other reasons in a typical April) had been classified as unemployed on temporary layoff, the overall unemployment rate would have been almost 5 percentage points higher than reported (on a not seasonally adjusted basis). However, according to usual practice, the data from the household survey are accepted as recorded. To maintain data integrity, no ad hoc actions are taken to reclassify survey responses (pp. 5-6).

As noted in the statement, they calculate that the unemployment rate would have been close to 20% if this data was accurately reported.

A second data point of note is that when those who are marginally attached to the labor force and the total employed part time for economic reasons are considered, the unemployment rate (technically referred to as U-6), was 22.8% in April (see Table A-15 in the report).

I hate to highlight more bad news, as if 14.7% of the labor force being unemployed was not bad enough, but in order to really understand the depth of the economic recession we are in, I think it is important to consider these figures.

Some definitions: Those marginally attached to the labor force include people who are not currently looking for a job but have indicated they would like to work and have looked for a job in the past 12 months. This also includes discouraged workers who have become discouraged about their prospects of finding a job and have dropped out of the labor force. Those employed part time for economic reasons are the workers who would like to work full time but can only find part time work.

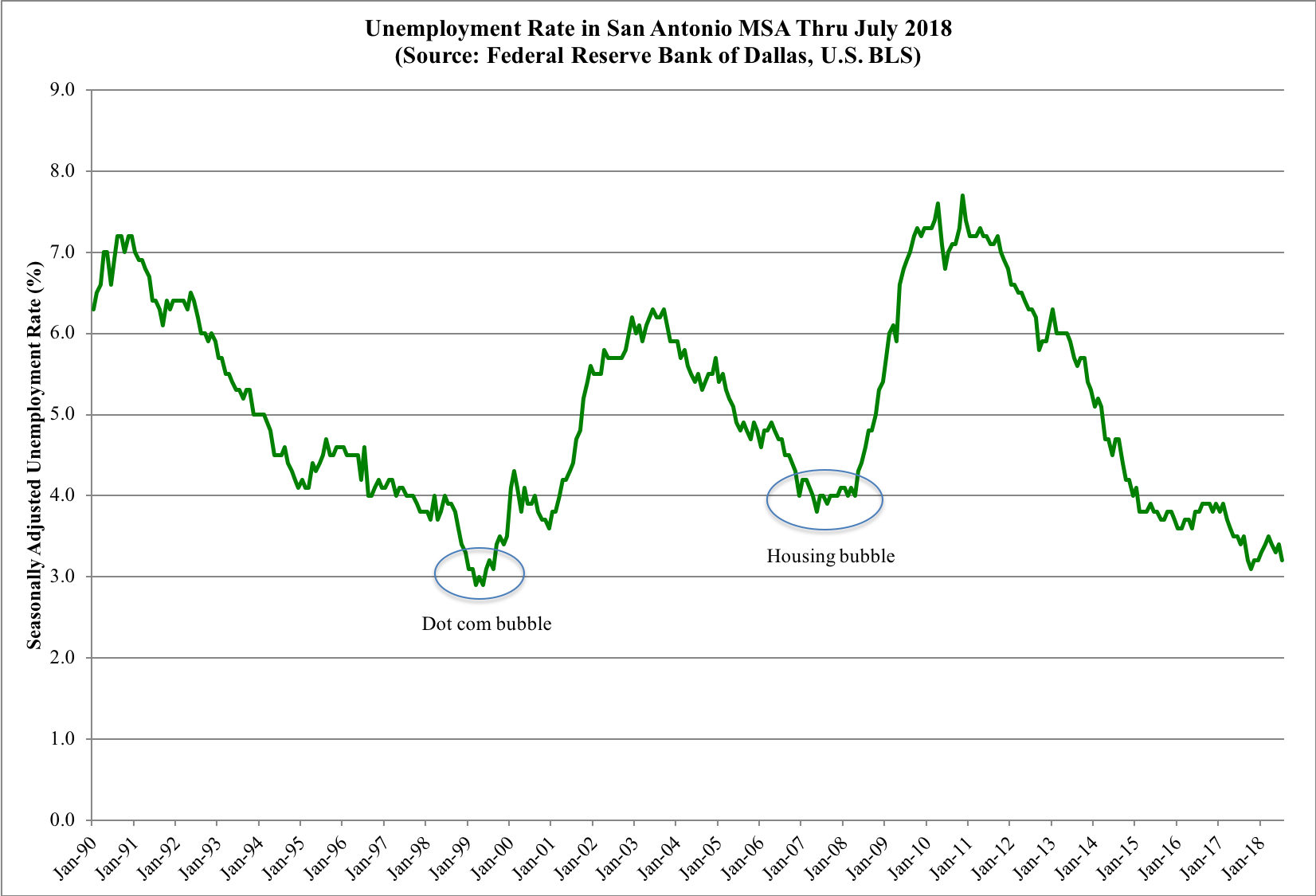

The unemployment rate in San Antonio in July was at a seasonally adjusted rate of 3.2%. Since May 2017, it has been in the range of 3.1-3.5% each month. This is about as low as the unemployment rate has ever been in San Antonio since January 1990, as far back as the data goes. The lowest it ever got was in March and May 1999 when it reached 2.9% in each of those months.

As shown in the graph, for about the past year, the unemployment rate has been near the level it was during the dot come bubble leading into the recession in 2000 and about one-half to almost a full percentage point lower than the unemployment rate during the housing bubble preceding the Great Recession.

It seems to me that the San Antonio economy has been at its full-employment level of unemployment, so it is most likely the unemployment rate will only be going up over the next year or so. It may continue to hover in the aforementioned range for several months, but it appears to have hit its floor.