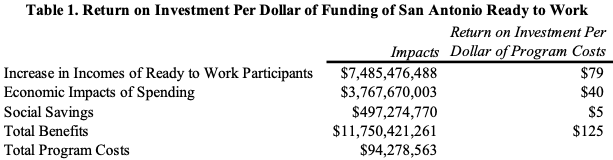

I recently completed a study of the economic impacts of the San Antonio Ready to Work program in collaboration with my colleague, Dr. Belinda Roman. The full report can be found here. The analysis projected the increase in incomes over the careers of those participants who completed their training and are placed into jobs, the economic impacts of the spending resulting from the increased incomes, and the savings to various social programs (e.g., Medicaid, WIC, TANF) that they will no longer need because of their increased earnings. These results are shown in the following table. The total benefits will amount to about $11.8 billion, and compared against the total program costs of $94.3 million, the return on investment will amount to $125 in benefits per dollar spent.

Investment in programs focused on workforce development like San Antonio Ready to Work are fundamental to the continued development of the San Antonio economy. Their importance may be enhanced in the future given the potential disruptive effects of AI on the labor market in the future.

Haven for Hope began operations in 2010 with the mission “to offer a place of hope and new beginnings by providing, coordinating, and delivering an efficient system of care for people experiencing homelessness in San Antonio.” Haven for Hope has become a model of excellence for how to establish and operate a facility to effectively and efficiently serve those who are experiencing homelessness. With its 75 partners and numerous volunteers,[1] Haven for Hope has provided care for 52,108[2] people who have experienced homelessness with profound impacts on their lives and the broader San Antonio and Bexar County community. For example, after one year upon graduating from Haven for Hope, 92.42 percent of those who exited to housing in 2023 remained in housing for at least twelve months through 2024. The retention rate for all of those who exited Haven for Hope and remained out of homelessness for at least twelve months, including those who exited to another facility for higher care, to stay with family or friends, to a transitional housing facility, and including all those who exited without completing an exit interview was 75.01 percent as of 2023. In part, this high housing retention rate is the result of the fact that 683 clients of Haven for Hope in 2024 found employment.[3]

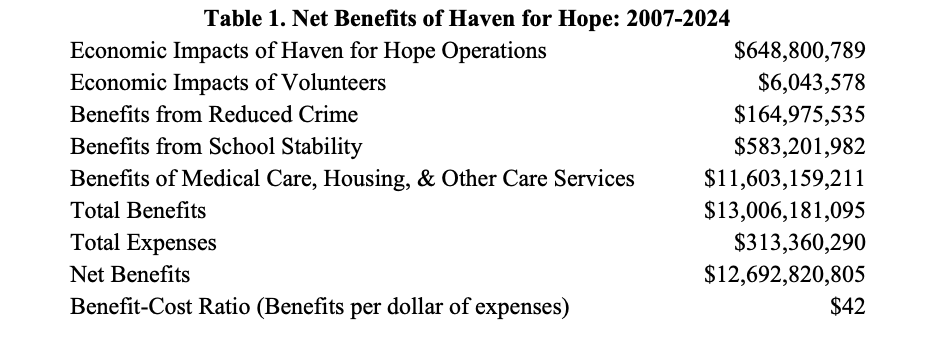

I recently completed a study to measure the net benefits of the services provided by Haven for Hope to the community from 2007 through 2024.[4] The value of the benefits and total expenses measured in the study are provided in the following table. Haven for Hope has provided net benefits to the community of $12.7 billion. In other words, for each dollar spent to create and operate Haven for Hope, the community has received $42 in benefits.

While the scope of this study only analyzed the benefits through 2024, it is also worth noting that Haven for Hope has continued to innovate and push its model of excellence in serving persons experiencing homelessness and the broader San Antonio community. This is exemplified through its contributions to the community’s response to the COVID-19 pandemic. While much of the community was in lockdown and experiencing unprecedented economic stress due to the pandemic, Haven for Hope made numerous adaptations to their operations in order to keep safely providing their services. This included the creation and implementation of Operation Hope Away from Haven focused on serving their highest-risk clients who had become exposed to COVID-19 and to maintain social distancing.

As these results indicate, Haven for Hope’s impact on the San Antonio community has been profound, especially for those they serve, but their overwhelmingly positive impacts extend well into the broader community. By providing a path to a new beginning for those who are experiencing homelessness, Haven for Hope’s work towards the achievement of their mission contributes substantially to both the quality of life of those they serve and all who live in San Antonio and Bexar County. By helping those persons experiencing homelessness find permanent housing and providing them with the care, guidance, and skills each individual needs to begin a successful journey to self-sufficiency, these benefits will be felt throughout their lifetimes and will also serve as a catalyst for economic development well into the future.

In the full report, the methodologies used in the analysis are documented and more detailed results are provided. If you wish to read the report, you can find it at this link.

[4] While operations did not begin until 2010, expenses to establish Haven for Hope began in 2007, so while the benefits were measured from 2010 through 2024, the expenses were calculated going back to 2007.

The Federal Reserve Bank of Dallas recently posted an interesting article in which it discussed the slowing growth in Texas as employment growth slowed in June. However, this has not been the case in the San Antonio-New Braunfels metropolitan area. As shown in the following chart, employment growth in San Antonio picked up pace in May and June in contrast to the state economy and the other major metropolitan economies in Texas. Employment growth in San Antonio was faster than all of the other major metropolitan economies but just slightly lower than the growth in the state. Employment across the state grew 1.64% while employment grew 1.59% in San Antonio in June (Table 1). While growth in San Antonio is relatively stronger than the other major metropolitan economies, it is still below the long-term average growth rate of 2.30%.

The figures in Table 2 show the growth rates by industry in San Antonio. The growth rates highlighted in green show those growth rates across each industry that accelerated during this time period. This shows that the employment growth in San Antonio over the three months from April through June have been driven by construction, mining, and natural resources; manufacturing; trade, transportation, and utilities; financial activities; education and health services; and leisure and hospitality. Construction grew on average 2.32% over this six-month period with the biggest acceleration coming in May and June, while mining and natural resources declined -0.45% over this period. For those who live in San Antonio, it is probably no surprise that construction drove the growth in this sector. Growth in education and health services was driven by growth in health services with an average monthly expansion of 4.09% over this period. Employment in private education health services shrank -1.88% on average each month. Keep in mind that this is just private education health services, as the public schools are captured in local government.

While the state and metropolitan economies are still expanding as measured by employment growth, their growth is slowing. Maybe San Antonio continues to lead the pack in growth, but I do expect overall growth to continue to be anemic and likely even slow more across the state and the U.S.

In my speeches, classes, or whenever I am asked about the state of the economy, I will frequently stress the need to look behind the headline economic numbers to get a better sense of what is happening in the economy and where it might be headed. This is arguably more important during these extraordinarily uncertain economic times, as illustrated by the current release of the U.S. real gross domestic product (GDP) figures.

U.S. real gross domestic product grew by 3.0% in the second quarter of this year. This follows a decline of 0.5% in the first quarter (U.S. Bureau of Economic Analysis). While the growth in the second quarter seems to indicate the economy has rebounded from the decline in the first quarter, it is necessary to look a bit deeper in the figures because these big swings in growth were driven by historically large changes in net exports. More specifically, it was large changes in imports as business substantially increased their imports in the first quarter to get ahead of the tariffs and then pulled back in the second quarter. This is shown in the following chart of the contribution in percent change in real gross domestic product attributed to net exports. The data in the chart go back to the fourth quarter of 1947 covering all data available, The contribution in percent change in real gross domestic product derived from net exports was -4.61 in the the first quarter of this year and 4.99 in the second quarter. It is clear from the graph that these are the largest swings in the contribution of net exports to the change in GDP in history. Net exports are the value of exports minus the value of imports, so the negative contribution of net exports in the first quarter is due to the very large increase in imports and the reverse of that in the second quarter.

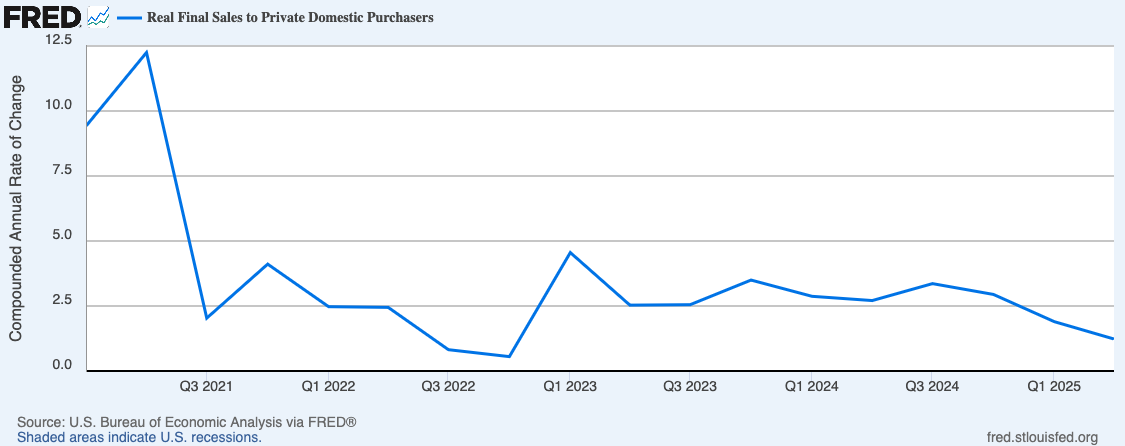

To get a clearer picture of how the economy grew over the first two quarters of 2025, we need to look at the change in real final sales to private domestic purchasers calculated as “the sum of consumer spending and gross private fixed investment [i.e., capital expenditures]” (U.S. Bureau of Economic Analysis). This removes the volatile components of GDP – net exports and inventories – and provides a “cleaner” measure of private domestic demand with a focus on domestic demand since net exports are removed.

The following graph shows the growth in real final sales to private domestic purchasers for each quarter since the first quarter of 2021. The picture of economic growth looks vastly different by this measure, since it has declined in each quarter since the third quarter of 2024. In the first quarter of 2025 real final sales to domestic purchasers grew 1.9%, but the growth rate declined to 1.2% in the second quarter (U.S. Bureau of Economic Analysis).

Contrary to what the headline GDP figures show for this quarter, trends in private domestic demand indicate U.S. economic growth may actually be slowing.

Haven for Hope sets the standard for helping those who are experiencing homelessness. With their partners and numerous volunteers, they have provided care to 40,000 individuals since they began operations in 2010. I was fortunate to have the opportunity to conduct a cost-benefit analysis of Haven for Hope covering the period of its founding in 2007 through 2019. The benefits measured in the study included the economic and fiscal impacts of Haven for Hope operations, the economic and fiscal impacts of the volunteers at Haven for Hope, benefits of reduced crime, benefits of providing school stability to children, and the benefits of medical care, housing, and other care services. Measured against the costs of developing and operating the facilities and programs, the net benefits the organization provides to the community are impressive.

Net benefits to the community ranging from $2.9 billion to $8.2 billion with an average of about $5.6 billion.

Benefits to the community per dollar spent ranging from $15.29 to $41.89 with an average of $28.72.

Haven for Hope has not only had profoundly positive impacts on those they serve, but the effects on the quality of life and the economy extend throughout San Antonio. The report discussing the impacts in more detail and documenting how the analysis was conducted can be found here.

The San Antonio economy has bounced back from the pandemic-induced recession quite nicely, and I believe the economy will likely continue to show growth at or slightly above its long-term trend in 2022. I project employment growth this year to be in the range of 2.2-2.7%, and the unemployment rate will continue to decline to about 3.5-4.0%. The data, trends, and potential factors that I am seeing in my crystal ball that form the basis for this forecast are discussed in the rest of this post.

After a quick rebound from the pandemic-induced recession, the San Antonio economy has moved toward its more long-term average growth rate in employment. This is somewhat against the pattern seen in the other major metropolitan economies across Texas, as they have continued to maintain historically strong growth. This is especially the case for the Austin economy. These patterns are evident in the following chart showing the year-over-year employment growth. Even though many of these areas have continued to experience such strong growth, it is clear that there is a sizable gap between them and the Austin economy.

As shown in Chart 2, the Austin economy grew 8.11% percent in December, which was still substantially larger than the second-fastest growing region – Dallas – at 5.82% and Fort Worth, the third fastest growing region at 5.02%. The San Antonio economy grew 2.87% in December – the slowest among the major metropolitan regions and below the growth rate across the state of 5.08% and the U.S. at 4.52%.

The large disparities in the growth of the Austin economy relative to San Antonio, and the other major metropolitan economies in Texas for that matter, is worth exploring, and I will have a post on that soon. For now, I want to focus on San Antonio.

Chart 3 shows the year-over-year employment growth by month across broadly-defined industries from January 2019 through December 2021 for San Antonio. As expected, the hospitality industry took the largest dive during the lock down followed by the professional services industry. These two industries have also had the largest immediate recoveries, along with the other services industry.

Chart 4 and Table 1 show the employment growth by industry from the depth of the pandemic-induced recession in April 2020 to a year later in April 2021, i.e., from trough to peak, and then for the remainder of 2021. It needs to be kept in mind that these are similar lengths of time, but it is clear from these numbers that the growth rates across almost all of the industries in San Antonio have slowed considerably. The manufacturing, construction and mining, and education and health industries have seen their growth basically stall or even turn slightly negative in the last three quarters of 2021. The one exception is the hospitality industry that not surprisingly continues to experience growth far above average.

Table 2 compares employment growth in San Antonio over its history leading up to the pandemic (Jan. 1991-Dec. 2019) to the growth rates across industries over the past year. Overall employment growth in 2021 was 2.87%, a bit above the historical average of 2.37% growth. Five of the ten industries – manufacturing; trade transportation, and utilities (TTU); professional services; hospitality; and other services – continued to grow at above average rates in 2021. Not too surprisingly, the hospitality industry continues to lead the growth with a rate of 10.87% in 2021 – far above the industry’s historical average. Only two industries experienced declining growth in 2021 – construction and mining and information. As shown in Chart 3, the declining growth in the information industry is a regression back to the mean based on recent history. Not to give away too much of the punch line for my next post, but this explains, in part, the difference in growth rates between Austin and San Antonio.

I expect these overall slowing trends in employment growth to continue through 2022 in San Antonio. Some of this is just going to be a regression back to the mean from the large growth rates as the economy recovered from the pandemic-induced recession. The structure of the San Antonio economy is an additional reason, and the potential effects of growth in the global and national economies will also play a role, as discussed below.

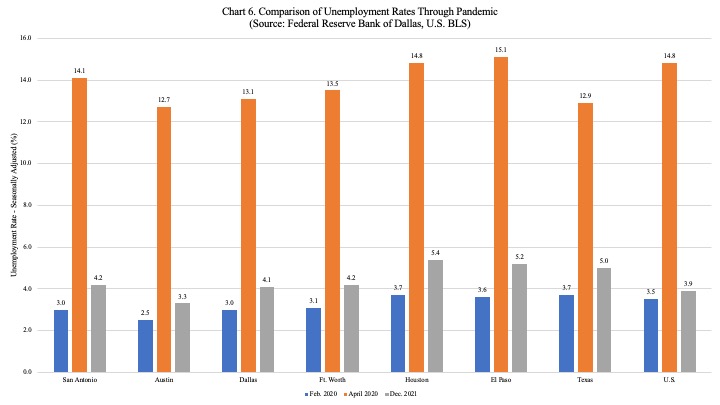

Similar to the pattern in the other major metropolitan Texas economies and across the state and U.S, the unemployment rate in San Antonio has steadily declined after the precipitous fall following the re-opening of the economy ending 2021 at a rate of 4.2% (see Chart 5). As shown in Chart 6, San Antonio had one of the lowest unemployment rates among the major metropolitan economies in Texas before the pandemic at 3.0%. However, San Antonio experienced one of the largest surges in its unemployment as it climbed to 14.1% in April 2020 at the depth of the recession, but as noted, unemployment has been consistently declining and is similar to the rate in Dallas (4.1%) and Fort Worth (4.2%). The unemployment rate in San Antonio is also lower than the statewide rate at 5.0%, but it is a bit higher than the U.S. unemployment rate at 3.9%. Compared to San Antonio, the unemployment rate in Austin was 0.9 percentage point lower at the end of 2021 at 3.3%. The strong economic growth since April 2020 has surely been the main driver pushing unemployment rates down, but it should be kept in mind that at least part of this decline may be due to the decline in the labor force participation rate due to the Great Resignation phenomenon. In fact, while the labor force participation has been increasing, it is still below the pre-pandemic rate of 63.4% in February 2020 for the U.S.

These structural changes in the labor market are one of the risk factors to this forecast. I can see these changes potentially having both positive and negative effects on economic growth. If the labor market adjusts to these changes fairly quickly and workers fill the jobs at higher pay and with enhanced benefits, this could serve as a boost to overall economic growth. However, if the current trend continues for an extended period of time, this could continue to exacerbate the shortages in many markets and serve to dampen economic growth. These adjustments in the labor market may be forestalled in industries where there is a relative paucity of benefits, such as paid sick leave. If the shortages causing the rapid increase in the inflation rate do not diminish in the near future, the persistent inflation at relatively high rates will also likely be a deterrent to growth in and of itself. In response to this, the Federal Reserve has sent strong signals that it will most likely be raising interest rates several times this year, which will also serve to slow the economy some. There could also be bubbles in many asset markets, such as the stock and housing markets, and if one or more of those bubbles burst, they might also cause the economy to pause a bit, even if it does not push it into a recession. The strong economic growth was, at least in part, driven by the federal government stimulus, and with that coming to an end, consumer spending is likely to move back into a more typical pattern over time causing a moderation in U.S. economic growth. It is also likely that growth in the global economy will also slow this year because of similar trends, and the economic effects of the war in Ukraine may also slow global economic growth a bit. Overall, it seems these various factors combined with the structure of the San Antonio will mean the local economy will continue to grow fairly strongly in 2022 but at a slower rate than in 2021.

I recently completed an economic impact analysis of the culinary industry in San Antonio in 2019 and 2020 for the San Antonio City of Gastronomy program. A summary of the results is shown in the following table. For the detailed results, please see the full report.

The culinary industry in San Antonio directly employed 125,770 workers and paid wages and benefits of $4,4 billion in 2019. The industry had a direct economic impact as measured by output of about $16.6 billion. The direct contributions to gross regional product (GRP) of the industry totaled $7.1 billion. However, with the impact of the COVID-19 pandemic, these impacts declined in 2020 with direct employment in the industry falling to 110,121 and wages and benefits declining to $4.0 billion. Direct economic impact shrank to about $15.8 billion, while the industry’s contribution to gross regional product fell to $6.5 billion.

When multiplier effects are included, the total employment supported by the culinary industry in San Antonio in 2019 was 227,764 workers who earned wages and benefits of almost $8.0 billion. The total economic impact on the local economy as measured by output amounted to $29.3 billion, and the industry’s contribution to GRP in 2019 was $13.4 billion. Like with the direct impacts, the total impacts declined in 2020. Total employment supported by the culinary industry declined to 208,642 jobs with incomes of $7.3 billion. The total output (i.e., economic impact) fell almost $1.5 billion to about $28.0 billion, and the total contribution to GRP declined 6.9% to $12.5 billion.

The Federal Reserve Bank of Dallas publishes a monthly report on San Antonio economic indicators, and in its most recent report, they published the following chart showing the fluctuations in restaurant reservations compared to 2019 in San Antonio and Texas. As they note, the demand for dining in restaurants fluctuates directly with the number of COVID cases, which accounts for the softening trend since June with the exception of the spike over Labor Day weekend. Another interesting trend the graph shows is the separation between dining demand in San Antonio and Texas over this past summer. Throughout the time period covered by the graph, the changes in San Antonio and Texas tracked very closely, but it seems the large amount of tourist activity in San Antonio over the summer generated a surge in demand for dining at restaurants in San Antonio over this past summer that was considerably larger than the activity across the state. It looks like the trend lines are back to moving more closely together following the Labor Day weekend and the return to school.

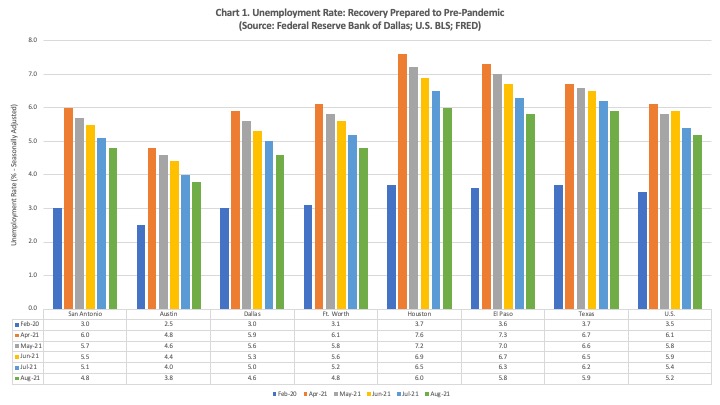

The unemployment rate continued its decline in August across the major metropolitan economies in Texas and across the State and U.S. as the recovery from the economic effects of the pandemic continue (see Chart 1). In San Antonio, the unemployment rate declined to 4.8%, This is 1.8 percentage points above the pre-pandemic level, so while the economy is certainly recovering, there is still a ways to go. San Antonio has the third lowest unemployment rate compared to the other major metropolitan economies in Texas with Austin having the lowest at 3.8%. The unemployment rate in Texas stood at 5.9%, a bit higher than the unemployment rate for the U.S. at 5.2%.

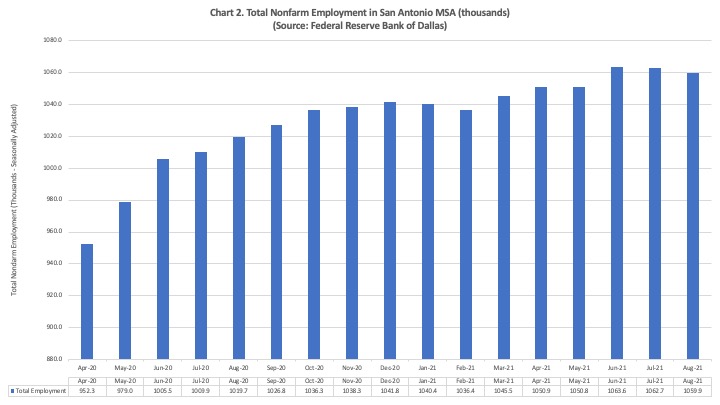

However, the total level of employment in San Antonio declined in July and August, as shown in Chart 2. This indicates to me that at least part of the decline in the unemployment rate in San Antonio may be due to people dropping out of the labor force and therefore, no longer being counted in the unemployment rate. This is also occurring in some of the other major metropolitan economies across the state.

While there have been monthly declines in total employment the past couple of months, the year-over-year growth rates in employment continued to be strong in August with growth in San Antonio coming in at 3.94% (see Chart 3), a good bit above the average historical growth rate in the region of about 2.3%. However, these growth rates continue to decline across most regions in the state, as well as across the entire state of Texas and the U.S. This is likely due to a regression to the mean as the recovery continues and some pull back in consumer spending due to the Delta variant. Another possible factor is the lag in business travel due to the pandemic. This especially affects those local economies with large leisure and hospitality industries like San Antonio because the convention activity is not filling in for the decline in leisure travel as the new school year began.

If we can keep making strides against the pandemic, growth should continue into the near future. This does not mean the year-over-year growth rates will increase, as they will likely tend to move more toward their long-term average rates in the respective areas as the economy gets closer to full employment. The sustained growth will also continue to push the unemployment rates down, especially as the structural unemployment is reduced.

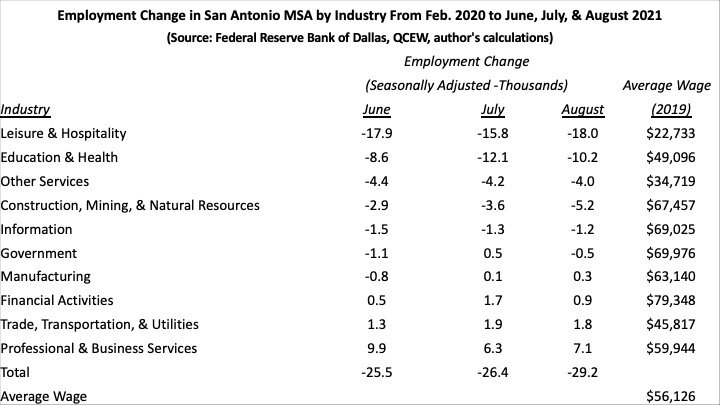

Employment in the San Antonio economy actually declined in July compared to June, as shown in the following table. Compared to the employment level in Feb. 2020, the month before the pandemic hit, employment in San Antonio was still down 25,500 jobs as of June and then in July decreased another 900 jobs to now being off by 26,400 jobs. The employment situation worsened in August as total employment was down 29,200 jobs compared to February 2020. These trends are probably reflecting many novel factors at play in the labor market, not only in San Antonio but across the U.S. and the world.

The unemployment rate in San Antonio has declined from 5.5% in June to 5.1% in July, and now it is sits at 4.8% in August. If the unemployment rate is going down while employment levels are also going down, this seems to me to indicate that the decline in the unemployment rate is due to people dropping out of the labor force instead of finding jobs. This may be due, in part, to the reduction/expiration of unemployment benefits, but it does not seem to indicate that the removal of those benefits had the large impacts on employment that some believed would be the case. Other factors seem to be driving workers’ decisions. Dr. David Autor puts forth an interesting explanation of what may be happening in his New York Times opinion piece (Autor, 2021). Regarding the effects of unemployment benefits, he refers to research showing that states which dropped the federal unemployment benefits this summer have seen very small declines in their unemployment rates. The Financial Times also recently published research on this same phenomenon (Smith and Zhang, 2021). Furthermore, Autor points out that Europe and Britain did not expand their unemployment benefits in a substantial way, and yet, they are also experiencing a labor shortage, too (Autor, 2021).

Having to put your son or daughter in child care has also been put forth as a possible explanation for the labor shortage, but as Autor notes, “women with children have since returned to work at almost the same rate as women without children, meaning access to child care isn’t the main culprit” (Autor, 2021).

He argues that the main reason for the labor shortage is “people’s valuation of their own time has changed.” In other words, many potential workers have decided that it is no longer worth working in a low wage job where they are also likely to be without benefits. As shown in the table above, those industries where wages are lowest are also those where there is high person-to-person interaction and thus, where workers are at increased risk of exposure to COVID. Instead, some are choosing to spend more time with their family and pursue other leisure activities that enhance their standard of living even if it reduces their incomes and consumption (Autor, 2021).

In addition to the explanation put forth by Autor, other factors may also explain what is happening in the labor market in San Antonio. It is clear in the table above that the leisure and hospitality industry and the education and health industry account for most of these job losses. As of June, leisure and hospitality accounted for 17,900 of the decline in jobs, and 8,600 of the jobs lost were in education and health. The employment situation improved in the leisure and hospitality industry in July where the reduction in employment compared to Feb. 2020 declined to 15,800, but the employment level worsened in August to 18,000 jobs. I think this may be due to the rather robust summer vacation season coming to an end followed by convention activity that is still depressed due to the pandemic. The situation got a bit worse in the education and health industry with employment being down 12,100 in July over this same time period but improved in August as the decline reduced to 10,200 jobs. The leisure and hospitality industry and education and health comprise a large part of the San Antonio economy. Besides the shift from leisure visitors to conventions as summer has ended that is possibly affecting employment in the leisure and hospitality industry, there is also much anecdotal evidence of workers in the leisure and hospitality and education and health industries leaving their jobs to seek employment in other industries for many of the reasons already stated. I suspect other metropolitan areas where these industries are a big component of the local economy are seeing similar effects.

It is also worth noting that in the industry that has shown the largest growth since Feb. 2020 by a wide margin, professional and business services, the growth declined from being up 9,900 jobs in June to only being up 6,300 jobs in July. Looking at the data on this industry in more detail, most of the decline occurred in the administration and waste services industry, for which I do not have an explanation. Employment levels did improve a bit in August with total employment in this industry being 7,100 jobs above the February 2020 level.

It is also important to keep in mind the wage levels of the workers most impacted by the economic effects of the pandemic. The average wage is presented in the table above and is calculated using data from the Quarterly Census of Employment and Wages for Bexar County. The average wage across all industries is $56,126 as of 2019, and of the four industries with below average wages, three of those industries are also the three most impacted by the pandemic in terms of declines in employment. This is no surprise as we have known that the economic effects of the pandemic have disproportionately fallen on those at the lower end of the income scale. As mentioned earlier, these are also likely to be the people most impacted by the loss of unemployment benefits, and given the other aforementioned factors at play in this labor market, it may also be deleterious to the overall economic recovery as their spending and engagement in the economy possibly declines.

Even more so, the adjustments happening on the supply-side of the labor market as discussed above indicate that the persistent labor shortage is due to structural changes, as workers reassess the value of their time and/or seek to transition to employment in different industries or different jobs in the same industry. The upshot is that the recovery back to pre-pandemic employment levels will take longer than if these effects were not occurring. This means that facilitating these adjustments is of utmost importance to helping those seeking to transition to new careers, but it is also vital to reducing the time it takes the economy to fully recover.